Optimize Your Loan Origination in CRE

Do you want to maximize efficiency and success in CRE lending with optimized loan origination processes? Discover how to streamline workflows and...

Learn the key steps in the CRE loan process with our guide for lenders to evaluate properties, borrowers, and risks to structure successful CRE loans.

The commercial real estate loan process has several key steps to get financing for commercial properties like office buildings, shopping centers, or apartment complexes. Unlike residential mortgages, these loans are designed for businesses, investors, and developers.

The process requires evaluation of the borrower’s creditworthiness, the property’s income potential, and the overall risk of the loan.

A smooth loan process benefits both borrowers (business owners) and commercial lenders through timely funding and structured financial agreements.

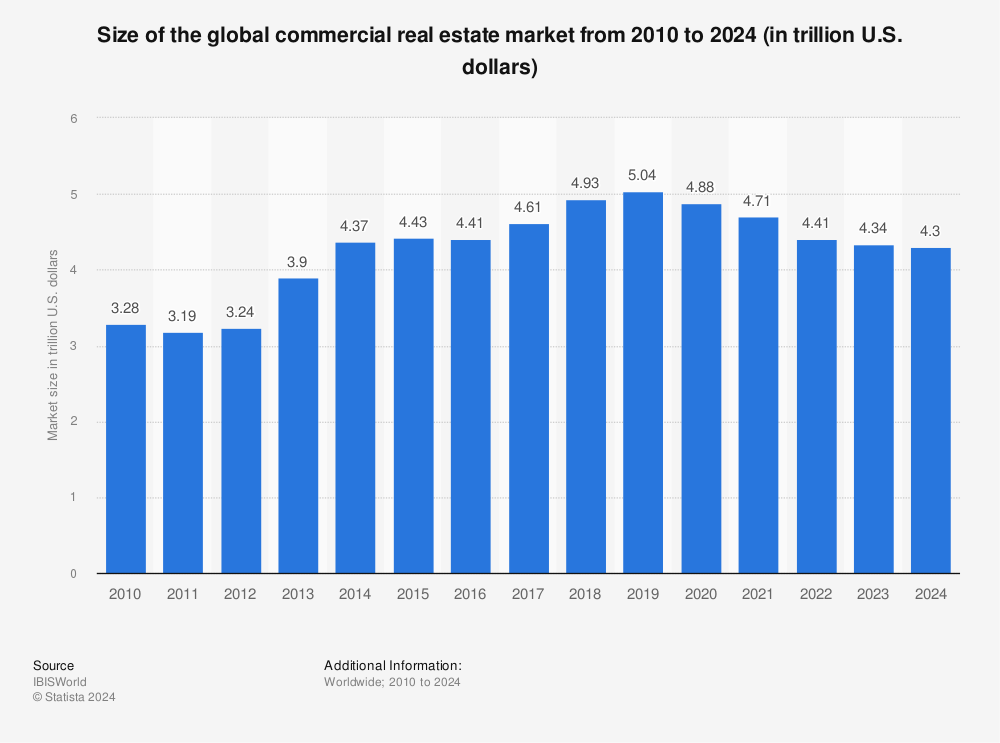

Did you know the commercial real estate market was worth well over $20 trillion last year? That’s a big chunk of the economy. So, you need to know how to navigate the loan process.

Source: Statista

In this post, we’ll cover the importance of commercial real estate loans, how commercial mortgage loans work from application to closing, what borrowers and lenders need to consider, credit history and credit rating, loan terms and cash flow, and how this can impact availing Small Business Administration/SBA loans, commercial bridge loans, and commercial hard money loans.

Let’s get into the comprehensive guide to the commercial real estate loan process and inform you how you can leverage Blooma in the process.

To navigate the commercial loan process with the best software, you need to know the key stages. These stages ensure both borrowers and commercial lenders are on the same page with the terms and viability of the loan.

Each stage is important to get a well-structured commercial mortgage loan, minimize risks, and set the stage for successful property investments. Here’s a breakdown of the main stages:

The borrower submits the commercial property loan application and supporting documents, financial statements, business plans, and income tax returns.

Pre-qualification is where the lender assesses the borrower’s creditworthiness and the loan-to-value ratio (LTV).

An appraisal is done to determine the commercial property’s market value.

This step ensures the purchase price matches the property’s actual value for the benefit of both the borrower and the commercial real estate lender.

During underwriting, lenders review the borrower’s credit history, cash flow, and the property’s income potential. The debt service coverage ratio (DSCR) is calculated to see if the borrower can cover loan payments.

Lenders also review all documents and verify everything during this stage.

Once underwriting is done, the lender gives loan approval.

Borrowers and lenders finalize loan terms, interest rates, repayment schedules, and prepayment penalties.

The last stage is signing all documents, paying closing costs, and disbursing funds.

This also includes paying legal fees so the loan is ready for the borrower to purchase or refinance the commercial property.

While the commercial real estate loan process is necessary to buy or refinance properties, traditional methods can be a big hassle that slows things down and increases risk.

In an industry where manual processes and inefficiencies are the norm, technology has become the game changer for the commercial real estate loan process.

Here’s how CRE software is addressing the challenges:

A faster commercial real estate loan process through mortgage lending solutions and other tech tools benefits all parties.

Here’s how:

In the cutthroat world of commercial real estate, a faster and more efficient loan process can make all the difference.

Blooma’s new approach uses technology to turn the commercial real estate loan process on its head and delivers benefits for lenders and borrowers alike.

Here’s how Blooma can revolutionize your workflows:

Wondering what the proof is to back this up? Request a case study so you can see firsthand how we’ve made a difference.

By using Blooma’s AI and digital workflows, lenders can speed up the commercial mortgage loan process, improve borrower experience, and reduce operational costs to win in today’s fast-paced real estate market.

A smooth loan process is key to success for both borrowers and lenders. By reducing delays and errors and improving collaboration, a smooth loan process creates faster access to capital and higher satisfaction for all parties.

Technology can do this. AI, automation, and digital platforms can speed up decision-making, reduce operational costs, and make the CRE loan process more efficient.

Blooma is leading the way in commercial real estate with AI-powered solutions to simplify underwriting, risk assessment, and loan management.

With Blooma, lenders can close more deals, borrowers can have a smoother experience, and the whole process is more transparent and efficient.

Find out how Blooma can transform your lending workflows.

Take the first step toward a faster, smarter, and more efficient CRE loan process with Blooma today!

Do you want to maximize efficiency and success in CRE lending with optimized loan origination processes? Discover how to streamline workflows and...

Master the art of portfolio lending in commercial real estate with Blooma’s comprehensive guide to optimizing your CRE loan portfolio for maximum...

Discover how embracing commercial loan automation can revolutionize your commercial real estate (CRE) lending and allow you to stay competitive in...